Stephen Takacsy, president, chief executive officer and chief investment officer, Lester Asset Management

FOCUS: Canadian stocks

MARKET OUTLOOK:

Stock markets have pulled back on fears of further rate hikes, recession and the recent failure of a few small regional banks which we believe are isolated cases. Bond markets continue to be very volatile and credit spreads have widened unnecessarily despite the economy being very strong. We believe that this volatility has presented some excellent buying opportunities in both stocks and bonds. In particular, corporate bonds are yielding “equity-like” returns of between six per cent and eight per cent, which investors should take advantage of since this won’t last. Inflation is coming down as supply chain issues ease and demand softens, and the rate hiking cycle is ending (it already has in Canada). If there is a pronounced recession or more turmoil in the banking sector, central banks might even cut rates which would cause a rally in both stocks and bonds.

We believe that in Canada and the U.S., there will be a “soft landing” as those economies are strong with low unemployment. Investor sentiment has been extremely bearish which is a great contrarian signal and as we know when sentiment starts to turn positive, markets usually rise sharply. This is why it’s important to stay the course. We remain nearly fully invested, but well diversified in recession-resistant businesses that are generating record profits. We also own many safe, high dividend-yielding companies like telecoms, pipelines, utilities and now banks which continue to look very attractive. We also own companies benefiting from long-term trends such as aging demographics (Savaria, Park Lawn, Neighbourly), digitization and automation (CGI, Tecsys, MDF, and ATS) as well as infrastructure (Stella Jones, AG Growth, Logistec). We also continue to take advantage of volatility to add high-quality companies at more reasonable valuations as share prices come down such as WSP, Colliers, and CCL).

Listen to the Market Call podcast on iHeart, or wherever you get your podcasts

Stephen Takacsy's Top Picks

Stephen Takacsy, president, CEO and chief investment officer at Lester Asset Management, discusses his top picks: High Liner Foods, Logistec, Definity Financial.

High Liner is a 120-year-old company that’s one of North America’s leading brands and processors of frozen value-added seafood to both food retailers and the food service sector. High Liner is the number one value-added player in Canada in the retail sector and the number one supplier in the U.S. in the food service sector. The industry is benefiting from healthier eating habits as more consumers add seafood to their diets, although per capita consumption in the U.S. is still very low.

Sales and EBITDA have been growing steadily over the past few years, and the company recently announced record sales and profits. It also just raised its dividend by 30 per cent (yields 3.5 per cent) which is a strong vote of confidence in the future. It expects to grow sales and EBITDA again in 2023 and generate significant free cash flow to pay down debt. Insiders own 40 per cent of the company, so have plenty of skin in the game. The stock is dirt cheap trading at around 7X earnings.

Logistec provides marine cargo handling services in 60 ports across North America including the largest container terminal in Montreal (load/unload cargo from ships). Business is booming in North American ports and they just announced its largest and most strategic acquisition yet giving them a strong presence in the Great Lakes. Logistec also has a fast-growing environmental business that provides soil and water remediation services and repairs water pipes and entered 2023 with a record backlog. The company just announced record profits of over $4 a share and is trading at a P/E of around 10X earnings and 6.5X EBITDA. The stock has rarely ever been this cheap. Multiples in the marine infrastructure and environmental businesses are significantly higher, and on a comparable basis, Logistec’s shares should be trading at around $80. The Paquin family owns a significant stake in the company and we would expect them to find ways of getting its share price to better reflect the company’s true value through aggressive buybacks and other means.

DFY is Canada’s sixth-largest property and casualty insurance company. Roughly 70 per cent of its policies are personal (auto, property and pet insurance) and 30 per cent commercial, mainly in Ontario. Roughly 60 per cent of its personal insurance is auto and it is looking to add more home and other types of insurance. It demutualized around 18 months ago by listing on the TSX, so it is not very well known compared to Intact Financial which is the number one player in Canada and also listed on the TSX. Despite growing faster than Intact and releasing strong results, its stock only trades at 14X earnings. It also trades at around 1.5X book value, a significant discount to Intact at 2.2X. Now that it is demutualized, it’s allowed to use its balance sheet to do mergers and acquisitions. With the recent pull-back, this is a great entry point to buy a fast-growing well-managed P&C company.

PAST PICKS: March 29, 2022

Stephen Takacsy, president, CEO and chief investment officer at Lester Asset Management, discusses his past picks: Pollard Banknote, AG Growth, and Steella-Jones.

This Saturn/Uranus cycle’s correlation with Finance has had a clear focus – the introduction of Deregulation and the consequences that have flowed from that culminating in the collapse of key banks and many financial institutions and the rescue of others by government and central banks. If this cycle opposition really does correlate with the Credit crunch then it is probable that the issue of how the Finance sector is effectively regulated will not be resolved till after the cycle Three Quarter stage between 2020 and 2023.

The present Saturn/Uranus cycle started recently in February 1988, reaching its outgoing square (+90 degrees) in 1999. The Opposition occurs from 2008 to 2011 and the incoming square (+270 degrees) will be reached in February 2021. (The next cycle will commence in June 2032,) What relationship between intellectual change and the status Quo does this cycle signify ?

What might the cycle mean ?

HOW A NEW MINDSET SWEEPS AWAY ESTABLISHED INSTITUTIONAL STRUCTURES

We have given the generic meaning of this cycle as the ‘Relationship between intellectual change and the Status Quo’. The term ‘Status Quo’ is a short way of saying ‘the established order of things’. ‘Intellectual’ should be taken to refer to reasoning and understanding – to ideas and not to something academic. Whereas the Uranus/Pluto cycle signifies how the structure and methods of intellectual, scientific, technological and aesthetic thought alter in themselves and the Uranus/Neptune cycle signifies how innovative ideas get taken up as ideals by society, the Saturn/Uranus cycle deals with how a new intellectual mindset actually alters or sweeps away established political, economic and institutional and other structures. It is all about ‘ideas in action’ or ’revolutionary ideas’ . We are talking of the emergence of a major new set of societal attitudes or new ideas leading to the break-up of political or socioeconomic structures.

Here we shall be looking at the conjunction for clear indications that new ideas are being born which show signs of changing or sweeping away established political, economic and other institutional structures. Throughout history this conjunction coincides with the overthrow of the establishment, typically governments or ruling parties but as we shall see sometimes even empires.

THE START OF A NEW CYCLE

CONJUNCTION Nov 1986 to Jan 1990, (exact in Feb, June and Oct 1988)

The 1988 Conjunction, allowing for a 10 degree orb, extends from November 30 1986 to January 3rd 1990. It coincides with one massive change to the established political and economic structure of the world – the collapse of the Soviet Union and the end of the Cold War. It also coincides with other regional events and developments which while not immediately related could be said to have been influenced ultimately by the same new mindset or wave of ideas.

These include the Tiananmen Square massacre in Beijing, China where troops kill 2,000 demonstrators, violent unrest in South Africa leading to a new President F.W. de Klerk lifting a ban on the African National Congress (ANC) and releasing its leader Nelson Mandela, and the exit of Russia from Afghanistan after 8 difficult years. There are also the overthrow of longstanding governments in the Philippines, Haiti, Fiji and Panama. In all these cases the attempt to overthrow the Status Quo was arguably influenced by the same set of ideas – those pushing a new wave of human rights, democracy and national self determination campaigns. In a sense the unusual number of peace agreements reached in 1988 between Ethiopia and Somalia, between Chad and Libya, between Egypt and Algeria and between Iran and Iraq could be said to reflect the same drive to allow new ideas to alter the status-quo.

FINANCIAL DEREGULATION – BIG BANG

BIG BANG

The second major correlation is with major shifts or changes to the Status-quo in the structure of institutions at the heart of the world economy. In particular, the 1988 Conjunction comes close to the end October 1986 deregulation of the London Stock Exchange – the so called ‘Big Bang’, which sees the whole established structure of city financial institutions change, and which results in a pay-out of such huge sums of money to partners and traders that the UK property market undergoes a period of wild inflation. A similar deregulatory move culminated in the United States in the same year. Amendments were made to Federal Reserve Regulation Q such that by April 1986 all interest rate ceilings had been eliminated except for the ban on demand deposit interest. The philosophy behind ‘Big Bang’ has much to do with the new economic strategy of ‘globalisation’ that is set to sweep the West. Again here is an idea that alters structures.

ASIAN ‘TIGER’ ECONOMIES

The period also sees the ascendancy of the Asian ‘tiger’ economies – Korea, Malaysia, Thailand, Taiwan and Indonesia, changing the geographical line-up of the established markets. Financial astrologers (such as Langham, Brahy and Jensen cited in Bates & Bowles’s ‘Money and the markets’) have consistently pointed to a correlation between the Saturn/Uranus cycle and economic activity – especially with investment in production. The correlation with the rise and fall of stockmarket prices however has been considered far less marked. Despite this in October 1987, during the period of the Saturn/Uranus conjunction, ‘Black Monday’ occurs – a day on which a massive stock market crash ends a period of marked economic growth and speculation. The effects of this ripple into the following year when the US dollar registers an all time low and when the New York Stock Exchange registers its third largest one day fall ever. Financial collapse on a far greater scale is due to take place precisely at a later stage in this Saturn/Uranus cycle !

DEREGULATION & GLOBALISATION

However it is not part of this book’s plan to examine any complex inter-relation between planetary cycles and stockmarkets or microeconomic conditions. The relationship, if it exists, is far more technical and statistical than this book aims to be or is qualified to cover. All that can be said is that structural changes in financial institutions as well as changes to the structure of international business play a key part in stockmarket volatility as evident in crashes such as Black Monday. Deregulation of the central money market in London and elsewhere is closely linked to globalisation. As we shall see later deregulation will be inextricably linked to the 2008 global ‘credit crunch’.

OTHER GEOPOLITICAL CORRELATIONS

There are three other key geopolitical developments between the end of 1986 and the end of 1989 which can be explained as structural changes resulting from a new collective mindset ? The developments are the Tiananmen Square massacre in Beijing, China where troops kill 2,000 demonstrators, violent unrest in South Africa leading to a new President F.W. de Klerk lifting a ban on the African National Congress (ANC) and releasing its leader Nelson Mandela and the exit of Russia from Afghanistan after 8 difficult years.

CONCLUSION

The key events correlating with this Saturn/Uranus conjunction are therefore the break-up of the Soviet Union and the fall of the Berlin Wall along with the deregulatory changes made to the structure of financial markets that accompany the emergence of globalisation. The suggestion is simple: there is going to be no structural change in society’s major institutions before the year 2032 (when the new cycle starts) that has not in some way got the imprint of these events on it.

OUTGOING SQUARE July 1998 to June 2001 (exact in July & Nov 1999 and May 2000)

Can we find in the relevant events and developments of 1999 and early 2000 a clear challenge or extension to the wave of ideas driving the overthrow of governments, institutions and practices inhibiting freedom which were seeded at the 1988 Conjunction ? The exact dates of the outgoing square are July and November 1999 and May 2000, but if we allow an orb of 10 degrees the period stretches from July 1998 to June 2001

DOTCOM CRASH

If the second most important development at the 1988 Conjunction was the Deregulation of financial institutions and the expansion of the number of investors, many of whom directly invested online in shares especially of the new technology companies, then the year 2000 certainly sees a major challenge to these developments – the ‘dotcom’ crash of April 2000. Though deregulation cannot be said to have led directly to the ‘dotcom’ crash, the ethos it inspired and the practices it encouraged certainly did. It is doubtful whether financial institutions would have piled into the ‘dotcom’ sector to the degree they did without the intensely competitive forces engendered by deregulation. It should be remembered that the 1988 conjunction also coincided with the ‘Black Monday’ stock market crash of October 1987. But the difference between the ‘Black Monday’ crash and the ‘Dotcom’ crash is important. The former was the result of a mixture of market forces, the latter was primarily the result of a combination of structural changes – in regulation, in the communications industry and in the investment community itself. And it is ‘Structural changes’ we are concerned with in this cycle.

ECONOMIC COLLAPSE THROUGHOUT ASIA

At the 1988 cycle conjunction we saw the rise of the Asian ‘tiger economies’ now in the years 1999 and 2000 we see an economic collapse throughout Asia as currency, share and property values plummet. The year had started with Japan reporting the most severe financial downturn in its post-war history. Then in April 1999, at the beginning of the Out square, China’s first major financial bankruptcy occurs as GITIC (Guangdong International Trust & Investment Corp) collapses with debts of US$4.5 billion – over the year China’s economy continues to deteriorate. In August the Ministry of Finance concedes that China is in recession with serious urban unemployment. In July 1999 Daewoo, South Korea’s second largest conglomerate, teeters on the brink of bankruptcy as management announces the corporation cannot meet the interest payments on its debt of a staggering $57 billion. Although in July 2000, as the Out square begins to move out of orb, it is generally concluded that the Asian economies had recovered from the crisis of 1998, the year 2000 sees economic stagnation continue in Japan. However the correlation is with emergent Asian economies and not the leading Far East economy.

CONCLUSION

The key developments at the Out square are twofold: first the appalling brutality in Chechnya and genocide in Kosovo is a severe challenge to the democratic and human rights optimism that accompanied the collapse of the Soviet Union and the end of the Cold War; second the challenge of the ‘dotcom’ crash to the forces unleashed by deregulation. Will the cycle opposition stage see some kind of maximisation of these developments ?

OPPOSITION Oct 2007 to Aug 2011 (exact in Nov 2008, Feb & Sept 2009, April & July 2010)

What developments might we expect to see at the Opposition in 2008, 2009 and 2010 when the contemporary movement for democracy and human rights together with the more deregulated investment scene should both reach a point of maximum fruition but where inherent contradictions may surface ?

The Opposition first comes into orb in mid October 2007 and stays in orb, with several short exit periods, through 2008, 2009 and 2010 up till August 2011.

FINANCE – THE CREDIT CRUNCH

TOXIC ‘SUB-PRIME’ LOANS

Only 5 days after the Saturn/Uranus Cycle Opposition first comes into orb on Oct 19 2007 Merrill Lynch reports its first quarterly loss in six years of $8.4 billion – on structured investment mortgage loans. In the days that follow Switzerland’s largest bank UBS, Japanese megabank Mitsubishi UFJ and Citigroup report similarly drastic losses on US ‘subprime’ loans. This kind of lending means making loans to people who may have difficulty maintaining the repayment schedule. These loans are characterized by higher interest rates, poor quality collateral and less favourable terms – in order to compensate for the higher credit risk. The losses are the first sign that many of such loans on major banks books are toxic – incapable of repayment.

That the message has not reached regulators is reflected by the Europe MiFID deregulatory directive issued on Nov 1 dropping some key rules on trading equities. On Nov 7 and Nov 20 Morgan Stanley and Freddie Mac, America’s largest buyer of home loans both report billion dollar losses from the same cause. On Dec 10 UBS says it will write off a further $10 billion of subprime losses. On Dec 20 Bear Stearns reports its first loss in its 84 year history. As the year ends the US Federal Reserve and the European Central Bank battle to shore up the money markets. In January 2008 Credit Suisse and Countrywide, the US’s largest mortgage lender, are hit by subprime losses while Citigroup and Merrill Lynch report historically unprecedented quarterly losses of $9.8 billion and $16 billion. On Feb 3 the cycle opposition goes temporarily out of orb.

In the seven months the cycle opposition stays out of orb what takes place in the banking markets is simply a consequence of what has already happened – a couple of further loss announcements, the injection by central banks of huge sums, the rescue by JP Morgan of US investment giant Bear Stearns and in Britain the nationalisation of mortgage lender Northern Rock.

BANKING TITAN LEHMAN BROTHERS GOES BANKRUPT

On August 29 the day the cycle opposition comes back into orb Integrity Bancshares becomes the tenth US bank to fail in 2008. But the full force of the returning cycle opposition explodes very shortly after on September 15 when the 158 year old banking titan Lehman Brothers, burdened by $60 billion in soured real-estate holdings, files for bankruptcy. It is the largest corporate failure in the history of the United States ! The markets go into terminal panic while the central banks desperately pump in billions of euros, pounds and in the case of the US Federal Reserve 70 billion dollars and a similar size loan to insurance giant AIG. By September 18 central banks around the world have poured in $180 billion to reassure the markets. The Russian government and the Bank of England together inject similar massive sums.While part of Lehman Bros is sold off, the other major US investment banks Morgan Stanley and Goldman Sachs defensively change their banking status.

CENTRAL BANKS INJECT $620 BILLION

On Sept 29 the US Federal Reserve with the help of the European Central Bank (ECB), the Bank of England and the Bank of Japan agree to lend banks a further $620 billion ! On October 1 2008 the US Congress signs off a $700 billion bailout of the financial industry. On Oct 8 six central banks cut interest rates together in an attempt to shore up confidence in the world’s crisis-stricken financial system with the US Federal Reserve reducing its key rate to 1.5%. On that day the International Monetary Fund (IMF) says the world economy is entering a major downturn. At the same time Iceland is obliged to take over the third largest of its banks while it negotiates a E4.5 billion loan from Russia. On Oct 10 as stocks crash to five year lows the Dow Jones index (DJIA) has its most volatile day ever and the London stock market plunges 10%. On Oct 13 as the central banks pump in further massive sums Wall Street rebounds in the biggest stock market rally since the Great Depression ! The EU/ECB alone puts $2.3 trillion on the line to protect its banks.

However on October 22 the DJIA tumbles 514.45 points – its 7th biggest point drop in history, as investors fear these moves will not prevent the global economy going into deep recession. The next day former Federal Reserve Chairman Alan Greenspan calls the current financial crisis a “once-in-a-century credit tsunami”. However on Oct 28 the DJIA rises 889 points, the 2nd biggest gain in its history. In December as the crisis spreads beyond banking the US administration is obliged to approve an emergency bailout of the US auto industry, offering $17.4 billion in rescue loans. The following month the UK Government will announce a similar measure. On January 1 2009 the Bank of America purchases investment giant Merrill Lynch to save it from bankruptcy. In February the US Treasury pushes out the boat further announcing a stimulus package that could amount to as much as $2.5 trillion.

UK’S ROYAL BANK OF SCOTLAND REPORTS £24.1 BILLION LOSS

In Europe a week later the Bank of England cuts interest rates to 1.5% – the lowest level since its founding in 1694 – it will fall a couple of months later to 0.5% and stay there. On Jan 14 2009 shares in Germany’s biggest bank Deutsche Bank slump as it posts massive losses. On Feb 13 the British Lloyds Banking group, already 43% state owned, announces a £10 billion loss at HBOS, a bank it had taken over four months earlier. But on Feb 13 the Royal Bank of Scotland reports a massive £24.1 billion loss – the largest in British corporate history – partly because of its mis-timed takeover of Dutch bank ABN Amro. In early March Eastern Europe’s struggling banks get a $31 billion loan. In April 2009 as the IMF forecasts losses from the credit crunch could reach $4 trillion, the Saturn/Uranus opposition goes briefly out of orb – till July 1st. During this gap there are no significant money market events.

BY 2009 GLOBAL CREDIT CRUNCH HAS COST $10 TRILLION

On 31 July 2009 the IMF states that the global credit crunch has cost governments more than $10 trillion. However in August France, Germany and Japan emerge from recession and in September some 27 central banks back new measures to strengthen supervision of the global banking industry – confirmed by the G20 summit on the 26th. On 15 October 2009 the DJIA index breaks through the 10,000 mark – the first time in a year. On Nov 13 the Eurozone economy emerges from recession. On Nov 19 the Organisation for Economic Co-operation and Development (OECD) says growth and recovery are expected in 2010 in just about all world regions. On Nov 27, as the Saturn/Uranus opposition goes out of orb again, US shares fall on worries about Dubai’s debt problems – accentuated by the refusal of the Dubai government to guarantee the debt. For bank debt is now no longer the key issue – the key issue is government debt – not least in the Eurozone area.

Read the book to see how the Eurozone crisis correlates closely with the remaining part of the Saturn/Uranus cycle Out square

This Saturn/Uranus cycle’s correlation with Finance has had a clear focus – the introduction of Deregulation and the consequences that have flowed from that culminating in the collapse of key banks and many financial institutions and the rescue of others by government and central banks. If this cycle opposition really does correlate with the Credit crunch then the health of the banking sector is unlikely to improve till the end of 2016 when the cycle reaches the unchallenging 240 degree stage. However it is probable that the issue of how the Finance sector is effectively regulated will not be resolved till the cycle In Square between 2020 and 2023.

The Saturn/Uranus incoming square came into orb on Jan 11 2020 and will last until 21 November 2023. The exact hits are in February, June and December 2021. Among the issues that have been correlated with this cycle since 1988 that of Financial Regulation and associated Finance market crises now appears top of the list. Between July and November 2020 any imminent eruption of a market crisis or regulatory move remains hidden but in November when the end of the global COVID-19 pandemic is in sight the result of the huge cessation of business and employment for so long is likely to ally with the increasing issue of government debt to lead to an upheaval in this area. Major Upheavals in Russia and China and possibly South Africa and Afghanistan may also be anticipated

A 45-year cycle of society and culture from 1988–2032

Are we witnessing the era of a New World Order?

The Mutilation of Uranus by Saturnby Vasari and Gherardi (16th century)

As I discussed at length in my recent article What’s Next: The Astrology of 2021, the major theme of this year will be the rather tense square aspect forming between Saturn in Aquarius and Uranus in Taurus. So I thought it might be beneficial to take a deeper dive into the symbolic relationship between these two planetary energies and examine the implications of this potent combination.

The Mutilation of Uranus by Saturn, depicted in the image above, is a 16th-century painting by Vasari and Gherardi that adorns the ceiling of the Room of Elements in the Palazzo Vecchio in Florence, Italy. It illustrates the Greek myth of the Titan, Saturn — the youngest son of the primordial god Uranus — in the act of castrating his tyrannical father with a sickle made of adamant (diamond), which was fashioned by his mother Gaia specifically for that purpose.

Entire volumes have been written attempting to unpack the complex symbolism and psychology of this succession myth. But for the purposes of this article, it provides us with a colorful backdrop for our discussion of the planetary archetypes that bear their mythical names.

For those who might be interested, I recently published an in-depth companion video on this subject of the Saturn/Uranus cycle on my YouTube channel.

Clash of the Titans

As planetary archetypes, Saturn and Uranus couldn’t be more different. They are in fact quite antithetical to each other, which is why the dynamic relationship of their cycle is so fascinating to observe. Saturn is the great boundary maker. It limits, restricts, confines. It is compelled to define and structure the world and bring order to chaos.

Uranus, on the other hand, revels in chaos. It is a most mischievous archetype that represents the urge to break free from all the limits, rules and restrictions imposed by Saturn. It is constantly bombarding Saturn with a relentless onslaught of revolutionary impulses, trying to break up all the crystalline structures that the old taskmaster has worked so hard to build, maintain and preserve.

Uranus wants to decondition us from all the conditioning patterns of life, family and society that Saturn represents. Why? Because it is an evolutionary necessity. In order to discover our true essential nature, we must progressively strip away all the conditioning patterns of our family, society and culture to find a deeper expression of the most unique and authentic aspects of ourselves — the core of our individual personalities. C.G. Jung referred to this as the process of individuation.

At their best, these two planetary archetypes combine to move society forward by means of slow and steady progress.

Depending on your own astrological framework, you may favor one side or the other in this cosmic battle between structure and reform, tradition and revolution, the safety and security of the past versus the risk and excitement of the cutting-edge future. Those of us with more Earth and Water in our birth charts may tend to be more risk averse and favor the Saturn side of the equation. Those of us with more Fire and Air may tend to be more risk-taking and embrace the exciting chaos of Uranus.

This tension between the archetypes of Saturn and Uranus often shows up as a “versus” dynamic:

conservative vs progressive

security vs adventure

age vs youth

materialism vs idealism

So we can expect these thematic tensions and energetic polarizations to be magnified within our culture this year. And keep in mind that the square aspect tends to constellate more of the shadow qualities of these two titanic archetypes.

At their worst, these two planetary archetypes can constellate and reinforce each other’s shadow aspects.

Synod: A Journey Together

The concept of a synodic cycle in astrology comes from the ancient Greek word synodos which means to “journey together.” So the synod of Saturn and Uranus outlines the roughly 45-year cycle of their journey together, and it’s influence is most acutely felt at its conjunction, square and opposition points — the so-called hard aspects. In 2021, we are experiencing what we call a “waning” or “last-quarter” square, marking the ¾ point in the 45-year cycle.

Typically, this period in any synodic cycle is associated with a crisis in consciousness. It represents the challenge of integrating what has been learned since the opposition of these two planets (which occurred back in 1999–2000). And that opposition represented the point of the greatest maturation in the entire cycle, where the original “seed idea” that was planted at the last conjunction (which occurred in 1988) came into its fullness.

So what was the original “seed idea” of this current cycle? In order to answer that question, we need to rewind to the beginning of this entire cycle, so we can understand the deeper meaning of this current crisis in consciousness.

American Global Hegemony

The current Saturn/Uranus cycle began with the last exact conjunction — which occurred in February of 1988 — when these two planets met at 29º Sagittarius. Of course, the beginning of a new cycle always signals the end of the old.

A linear mapping of the current cycle, highlighting the four “hard aspects” and their positions in the zodiac.

The previous cycle (from 1942–1988) perfectly bookended the Cold War Era — from World War II to the fall of the Berlin Wall. In the late 1980s, it seemed as if the USA had clearly won the decades-long Cold War, with its adversary, the USSR, having crumbled from within. America was emerging victorious as the sole global power.

A new era was beginning.

At its best, the initiation of a new Sa/Ur cycle represents the ability to take bold new inventions and innovative technologies (Uranus) and harness them in productive and lasting ways within society (Saturn). When they form a conjunction, they conspire to “birth’’ or “seed” a new vision that reflects the qualities of the sign in which they conjoin.

So we can frame this current cycle as one that began in the sign of Sagittarius, and is encapsulating a period of global expansion that has created a deeply interdependent global economy and a deeply interconnected global information ecology (via the internet). The notion of a Global Village first articulated by the famous media theorist Marshall McLuhan in the 1960s has now become our planetary reality.

Some very “global” seed ideas were planted during the Sa/Ur conjunction that occurred in expansion-minded and worldly-oriented Sagittarius in 1988.

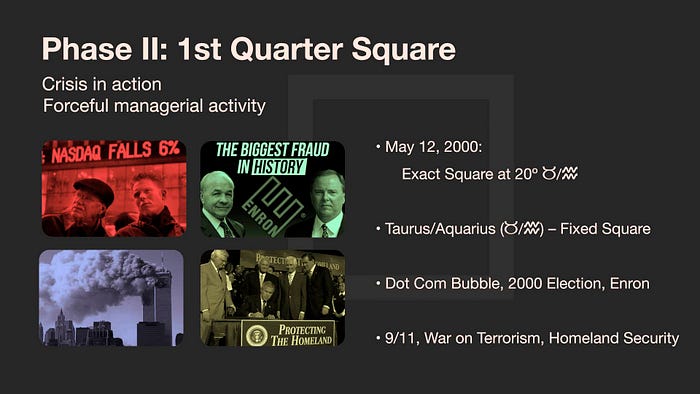

Crisis in Action

The energy initiated during the conjunction in Sagittarius in 1988 would have come into its first hard aspect during its first quarter square in the year 2000, when Uranus had moved into Aquarius and Saturn into Taurus. The incredible period of technological innovation and global expansion that occurred throughout the decade of the 1990s (with Uranus moving through Capricorn and then Aquarius) created a dot-com bubble, which suddenly burst when Saturn (limits and restrictions) came into a hard square aspect in the sign of Taurus (resources and finances).

This first quarter square created a crisis in action and required a necessary adjustment. The unbridled enthusiasm of the early phase of the cycle needed to be harnessed into more practical and sustainable structures. Keep in mind that this was also during the period of Pluto’s transit through Sagittarius (1995–2008), so the energy pattern for global expansion was incredibly accelerated during this period.

But the dot-com bubble is clearly connected to the Saturn/Uranus (Sa/Ur) cycle. Particularly, this era of America’s global hegemony, which has been bolstered as much by technological innovation as by military might, witnessed the center of economic power shift from the industrial military complex of the previous cycle, to Silicon Valley and the tech giants of the current cycle.

From the perspective of the Sa/Ur cycle, we can see this first quarter square in the year 2000 as a point of adjustment: a revaluing and retooling of the entire tech sector. The next phase in the cycle would witness the potent combination of wireless networks and smartphone technologies that pushed the internet age to new heights.

The disruptive effects (Uranus) of the nascent app-based economy would prove to have monumental consequences for more traditional providers of goods and services (Saturn). The disruption of online retailers to traditional brick & mortar outlets was overwhelming. Over this period businesses like Barnes & Noble, a literal cornerstone of the retail space, would all but disappear in the face of competition from online bookseller Amazon, which ruthlessly leveraged its massive asymmetrical advantage to gobble up other areas of the retail space as well.

Disrupting The Grid

Another common manifestation of the Saturn–Uranus interface can be witnessed in disruptions to the energy grid. The rolling blackouts during the 2000–2001 square aspect that led to the California electricity crisis were a perfect example of this phenomenon. A myriad of factors were to blame, including a drought, lack of new capacity and market manipulation.

The last of those factors was directly connected to the Enron scandal that occurred during the same time period. The energy giant’s complex financial scheme was exposed as a massive fraud. The company went bankrupt and a few executives went to jail. But electricity consumers—mostly Californians—were left holding the bag. This is a common theme that tends to play out over the course of this push/pull, expansion/contraction cycle, as we’ll soon see.

Does any of this sound familiar? Should we consider the most recent Texas power crisis of 2021, when more than 4.5 million homes and businesses were left without power… in the dead of winter… during a pandemic? Yeah, these cycles tend to repeat themselves. It seems the current square aspect of 2021 is starting to feel a lot like the last square aspect of 2001. And as we’ll see, the parallels are becoming eerily similar.

Pluto Enters The Picture

By the middle of 2001, Saturn was moving beyond its square aspect with Uranus. But it was headed straight for another difficult encounter—an opposition with Pluto. The Saturn/Pluto cycle is yet another pattern of great significance in our world, one characterized by war, violence, terrorism and disease. And it illustrates how often these planetary cycles can intersect and overlap, sometimes with far-reaching and often devastating consequences.

On September 11, 2001, Pluto (planet of chaos and destruction) was in Sagittarius (sign of religious fanaticism), while Saturn (planet of rigid authority) had moved into Gemini (the Twins). How’s that for archetypal symbolism expressing itself?

In two years—from 1999–2001— a chain reaction between Uranus, Saturn and Pluto had triggered a major shift in geopolitics. The War on Terrorism, the Department of Homeland Security, the Transportation Security Administration, the Iraq War, the rise of the surveillance state— the world has really never been quite the same since. And the impact of this triple triggering transit—with Pluto interfacing the Saturn/Uranus cycle—would continue to exert a disruptive and transformational force.

During the 1st quarter square in 2000, the globalist cycle encountered its first test—a crisis in action.

American Dream or Financial Ruin?

The next major aspect came in 2009 with the opposition of Uranus in Pisces to Saturn in Virgo. This exactly coincided with the height (or rather depths) of the Great Recession that resulted from yet another bubble — this time the one created by the subprime mortgage scandal that resulted in the housing crisis.

Considered to be one of the greatest economic disasters in US history (second only to the Great Depression), the fallout from this crisis spread around the world, exposing just how interconnected — and perilously fragile — the global economy had become. Reflecting back on the fact that this cycle began in Sagittarius, we can understand how this opposition reveals the maturation of the “seed impulse” towards globalism that was implied by the original conjunction in 1988.

It’s also interesting to note that the opposition occurred while Uranus was in dreamy and deceptive Pisces, expressing both the American Dream of owning your own home and the deceptive practices of the investment banks and financial institutions who knowingly packaged these low-grade and risky investments and labelled them as A-1 quality. The bankers were using high-tech and extremely complicated financial instruments (Uranus) that even they didn’t fully understand (Pisces). In a classic expression of the opposition aspect, we had become divorced from reality.

So when Saturn moved into opposition in practical and detail-oriented Virgo, and the lawyers and accountants came in to analyze the nitty-gritty details of the “cooked” books of the investment banks, they quickly realized they were in way over their heads, and that entire global economy was about to come to a screeching halt.

But a new concept was born from this crisis: too big to fail. Now, if that doesn’t have the fingerprints of Saturn conjunct Uranus in Sagittarius all over it, I don’t know what does. But it really does set a dramatic stage for the theme of the second half of this cycle. When we unpack this concept, we see that when something is too big (Sagittarius) to fail (Saturn), it’s going to require some massive reform (Uranus) in order to survive, otherwise it will likely be destroyed (Pluto).

Again, I’ve interjected Pluto into this formula, because it continues to be a major player in this unfolding Saturn/Uranus story. Coincidently, Pluto moved from Sagittarius into Capricorn at the exact time the Great Recession was imploding in 2008. So the symbolism of Pluto (the impulse for necessary change and evolution) moving from Sagittarius (global expansion) to Capricorn (social structures, institutions and hierarchies) highlighted a need for necessary reforms to the system in order for society to continue to evolve.

But those reforms never happened. The Federal Reserve printed a few trillion dollars out of thin air, and everyone pretended to go back to business as usual. The problems and inequities inherent in the underlying fundamentals of the global economy that were laid bare by the events of Great Recession were never properly addressed.

As Pluto has continued its journey through Capricorn, all the various systems and institutions that make up the global economy have been increasingly stress-tested. Keep in mind that Pluto tends to elicit evolutionary change in one of two ways: either by slow and deliberate evolution through cooperation and conscious effort, or by sudden, catastrophic destruction and havoc wrecked by unconscious impulses. Which side of that equation does it feel like we are embracing?

During the opposition in 2008–2009, we lost our focus and became deeply divided.

Crisis in Consciousness

Now in 2021, we are entering the last quarter square phase of the synodic cycle between Saturn and Uranus, which is characterized by a crisis in consciousness. What’s required to handle the current situation is not so much new actions, but new ways of thinking. During the opposition of 2009, we were shown how dangerously divorced we had become from reality, revealing a world increasingly divided between haves and have nots, the 1% versus the 99%.

There’s an interesting symmetry between this last quarter square we are entering now in 2021 and the fist quarter square we endured back 1999–2000. At that time, Uranus was in Aquarius and Saturn was in Taurus. This time, it’s the other way around — Saturn is in Aquarius and Uranus in Taurus. Might we expect some sort of role reversal?

During the tech bubble of 2000, what was disrupted (Uranus) was Big Tech (Aquarius), which caused limits and losses (Saturn) to the financial markets (Taurus). This time around, a scenario could play out where the disruption (Uranus) will occur in the financial markets (Taurus), causing limits and losses (Saturn) to Big Tech (Aquarius).

Could the Big Tech platforms be in for a rude awakening this year? Or have they become — like the out of control investment banks in 2009 — too big to fail? It seems counterintuitive to think that tech stocks — now riding all time highs in the current (and highly irrational) bull market — could somehow suffer the limits and losses often imposed by Saturn during these triggering transits. But stranger things have happened, my friends.

What’s that old saying on Wall Street? Bulls make money. Bears make money. Pigs get slaughtered.

Mad Money

Another area that could be up for disruption and sudden change is the entire global monetary system itself. With central banks printing trillions of dollars out of thin air under the auspices of “quantitative easing,” and crypto fever pushing Bitcoin over $50,000, the climate seems ripe for some kind of showdown between traditional fiat currencies and the emergent digital coin culture. This is classic Saturn/Uranus.

The two recent events that most characterized this archetypal complex are the Capitol Riot (irresponsible or harmful forms of rebellion) and the Gamestop phenomenon (challenging the bedrock assumptions of a worldview).

Both may be harbingers of things to come.

The “Big Brother vs. Little Brother” theme of Saturn and Uranus seems to constellate just these types of scenarios. More often than not, the Uranian or Promethean-like hero figures end up being subdued by the Saturnian or Authoritarian-like powers that be. But in this new Aquarian Age, might those tables be turning?

There are a lot of big ideas and big numbers being floated. Infrastructure packages exceeding $2 trillion. Great Resets and Green New Deals. Debt jubilees, indigenous reparations and universal basic income.

Many of the major decisions that are made in the next few years will determine how this entire 45-year cycle will end. We likely won’t know the true outcome until 2032, when the current cycle concludes and a new cycle begins. The next conjunction will occur in the sign of Gemini — certain to usher in a future era mediated by exponential advancements in information technology. Will it look more like a decentralized, equitably-distributed and inclusively-oriented global village — one that restores the tragedy of the commons? Or will it devolve into a dystopian prison planet dominated by Big Brother and Big Tech — one that perpetuates the zero sum game of a voracious global technocracy?

We are about to find out.

During the last quarter square from 2020–2022, we are being challenged with a crisis in consciousness. Can we think our way out of this mess?

Resolving Internal Conflicts

2021 will continue to be a year dominated by this square energy. We have Uranus in Taurus — a progressive planet in a rather conservative sign, in square with Saturn in Aquarius — a conservative planet in a rather progressive sign. So we can expect a lot of tension (square energy) between progressive and conservative impulses throughout the remainder of 2021. This will likely play out on the political stage and continue to ripple through the culture at large. Additionally, each of us as individuals will likely feel this tension internally as well as interpersonally.

Many of us are internalizing the push/pull dynamic of this current energy pattern. We are torn between clinging to our past and traditions (Saturn) and embracing what seems like a necessary and inevitable future (Uranus). Any cursory cruise through any of our social media feeds will show us this tension playing out in real time amongst our friends, family and colleagues. We’re all in the midst of a crisis in consciousness. So what is the best course of action to navigate this current crisis?

When we consider the best qualities of the archetypal Saturn/Uranus complex, we are encouraged to pursue the paths of responsible freedom, cautious innovation and liberation through everyday routines. None of it is super sexy, but it does contain the kind of sober medicine and healing elixir that is necessary for the times.

When properly and potently combined, the archetypes of Saturn and Uranus arm us with the courage to challenge the bedrock assumptions of our worldview. What is wrong, or simply outdated in our approach? What new perspective is required to continue to evolve and innovate? How can we extricate ourselves for the problem — solution — more problems trap? How do we embrace the dialectic process of moving beyond thesis and antithesis, and shift into some new synthesis?

There are no easy answers. There rarely are during difficult or challenging times. These are times of character testing. These are times to dig deeper. These are the times that try our souls.

We have crossed a threshold. We have entered into the Aquarian Age in earnest. We opened a cosmic and collective doorway during the Great Mutation that occurred in Aquarius on the Winter Solstice last December. With Uranus as the modern ruler of Aquarius, and Saturn as the traditional ruler, the combined planetary energies certainly align with Aquarian values. The question is: which aspect of the Aquarius archetype will we embrace? The positive side of responsible freedom and cautious innovation? Or the shadow side of extreme polarization and rude awakenings?

There will be two more exact squares of Saturn and Uranus this year — on June 14th (with Saturn retrograde) and again on December 24th (with Uranus retrograde). Regardless of which side of the equation manifests, we can all expect to feel an acceleration of the acute tension between conservative and liberal elements, between materialism and idealism, between past comforts and future needs — both in ourselves and in the world at large. And we will all be required to reconcile these tensions within ourselves. May we endeavor to do so with the courage of love and the humility of necessity.

Sat Nam, everyone.

Daljeet Peterson, May 6, 2021

Want to explore the topic further? Check out my in-depth companion video on this subject of the Saturn/Uranus cycle on my YouTube channel. Hope to see you there too!-----------------------------------------------------------------------------Source https://medium.com/astrolab21/the-saturn-uranus-cycle-clash-of-the-titans-9fc789e3b738