Treasury bond yields (or rates) are tracked by investors for many reasons. The yields are paid by the U.S. government as interest for borrowing money via selling the bond. But what does this mean, and how do you find yield information?

Treasury Bills are loans to the federal government that mature at terms ranging from a few days to 52 weeks.1 A Treasury Note matures in two to 10 years, while a Treasury Bond matures in 20 or 30 years.23

The 10-year Treasury yield is closely watched as an indicator of broader investor confidence. Because Treasury bills, notes, and bonds carry the full backing of the U.S. government, they are viewed as one of the safest investments.4

Key Takeaways

- Treasury securities are loans to the federal government. Maturities range from weeks to as many as 30 years.

- Because they are backed by the U.S. government, Treasury securities are seen as a safer investment relative to stocks.

- Bond prices and yields move in opposite directions—falling prices boost yields, while rising prices lower yields.

- The 10-year yield is used as a proxy for mortgage rates. It's also seen as a sign of investor sentiment about the economy.

- A rising yield indicates falling demand for Treasury bonds, which means investors prefer higher-risk, higher-reward investments. A falling yield suggests the opposite.

Why Is the 10-Year Treasury Yield So Important?

The importance of the 10-year Treasury bond yield goes beyond just understanding the return on investment for the security. The 10-year is used as a proxy for many other important financial matters, such as mortgage rates.

This bond also tends to signal investor confidence. The U.S Treasury sells bonds via auction and yields are set through a bidding process.5 When confidence is high, prices for the 10-year drop and yields rise. This is because investors feel they can find higher-returning investments elsewhere and do not feel they need to play it safe.

But when confidence is low, bond prices rise and yields fall, as there is more demand for this safe investment. This confidence factor is also felt outside of the U.S. The geopolitical situations of other countries can affect U.S. government bond prices, as the U.S. is seen as safe haven for capital. This can push up prices of U.S. government bonds as demand increases, thus lowering yields.

4 Types of Treasury Debt

The U.S. Department of the Treasury issues four types of debt to finance government spending: Treasury bonds, Treasury bills, Treasury notes, and Treasury Inflation-Protected Securities (TIPS). Each varies by maturity and coupon payments.3126

Another factor related to the yield is the time to maturity. The longer the Treasury bond's time to maturity, the higher the rates (or yields) because investors demand to get paid more the longer their money is tied up. Typically, short-term debt pays lower yields than long-term debt, which is called a normal yield curve. But at times the yield curve can be inverted, with shorter maturities paying higher yields.

Economic Indicator

The 10-year Treasury is an economic indicator. Its yield provides information about investor confidence. While historical yield ranges do not appear wide, any basis point movement is a signal to the market.

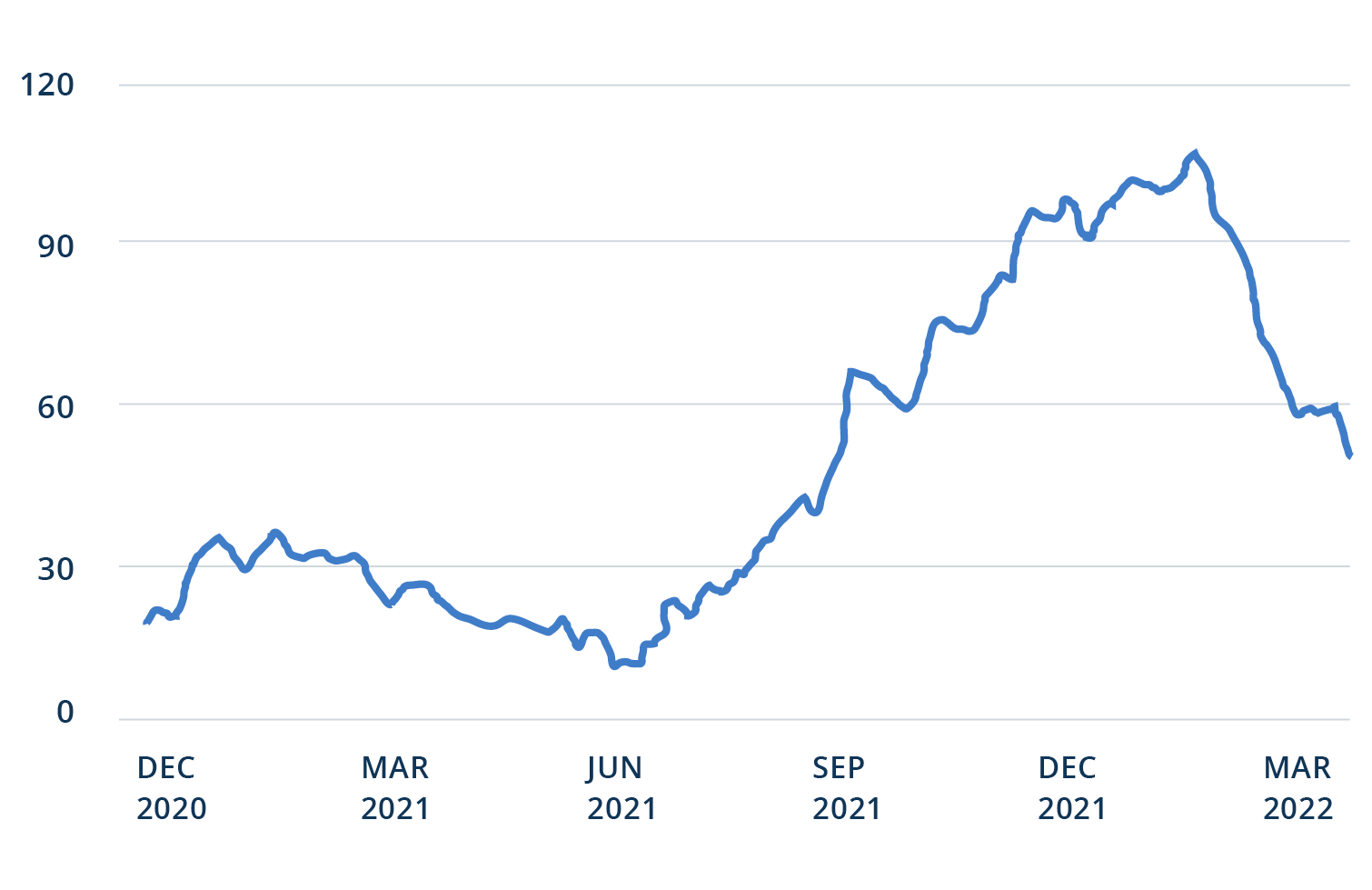

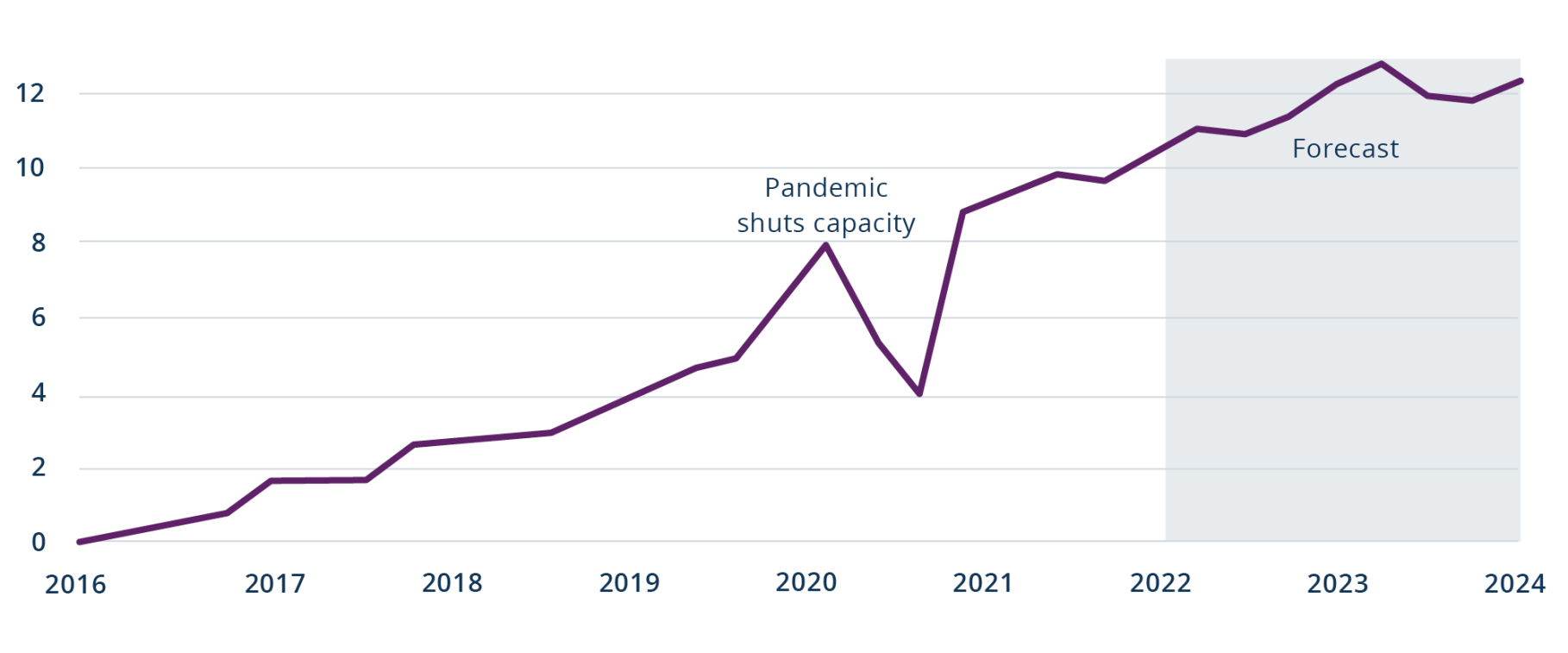

Changing Yields Over Time

Because 10-year Treasury yields are so closely scrutinized, knowledge of its historical patterns is integral to understanding how today's yields fare as compared to historical rates. Below is a chart of the yields going back a decade.

While rates do not have a wide dispersion, any change is considered highly significant. Large changes of 100 basis points can, over time, redefine the economic landscape. The yield curve has been flattening at an accelerated pace, which could be construed as a worry over economic growth and investor uncertainly regarding monetary policy.7

Perhaps the most relevant aspect is in comparing current rates with historical rates, or following the trend to analyze whether near-term rates will rise or fall based on historical patterns. Using the U.S. Treasury website, investors can easily analyze historical 10-year Treasury bond yields.

Factors that Affect the 10-Year Treasury Yield

There are many factors that affect the 10-year yield, the most substantial being investor sentiment. When investors have high confidence in the markets and believe they can profit outside of Treasury securities, the yield will rise as the price falls. This sentiment is determined by both the individual investor and investors as a whole, and can be based on any number of factors such as economic stability, geopolitical fluctuations, war, and more.

A decline in the 10-year yield indicates caution in the markets and the future of the global economy. Conversely, gains in the yield signal confidence.8

Interest rates are another significant factor. Since they are the benchmark from which all other rates are derived, they have a direct impact on yields. When the Federal Reserve lowers its key interest rate, it drives demand for Treasury securities.

Inflation has an effect on yields as well. Treasury yields rise when fixed-income products become less desirable. Over time, central banks will adjust (raise) their interest rates to combat inflationary pressure.

Can You Lose Money on Treasury Bills?

The short answer is no, as your principal is protected by the government. However, Treasury bills are highly subject to inflationary pressure. If an investor were to purchase a bond today, and then inflation picks up, the purchasing power of their principal will be severely diminished by the time their security reaches expiration. Even though that investor receives their principal plus interest, they are in effect losing money due to the money being worth less when they withdraw it.

What Does the 10-Year Treasury Yield Mean?

The 10-year Treasury yield is the yield that the government pays investors that purchase the specific security. Purchase of the 10-year note is essentially a loan made to the U.S. government. The yield is considered a marker for investor confidence in the markets, shining a light on whether investors feel they can make a higher return than the yield offered on a 10-year note by investing in stocks, ETFs, or other riskier securities.

What Factors Affect the 10-Year Treasury Yield?

Some factors that affect the 10-year Treasury yield are inflation, interest rate risk, and investor confidence in both the Treasury security and the overall economy.

The Bottom Line

The 10-year Treasury yield is used to determine investor confidence in the markets. It moves to the inverse of the price of the 10-year Treasury note and is considered one of the safest—if lowest returning—investments that can be made. Although the investment is guaranteed by the U.S. government, investors could still lose money if inflation outpaces the 10-year yield.