Transport Infrastructure: Four Themes to Watch

Introduction

The steady stream of news about supply chain bottlenecks has put a spotlight on the essential nature of transport infrastructure and logistics assets around the world.

While the peak of the supply chain disruption is likely behind us, it exposed problems that persist, such as outdated infrastructure and insufficient capacity, flexibility and efficiency.

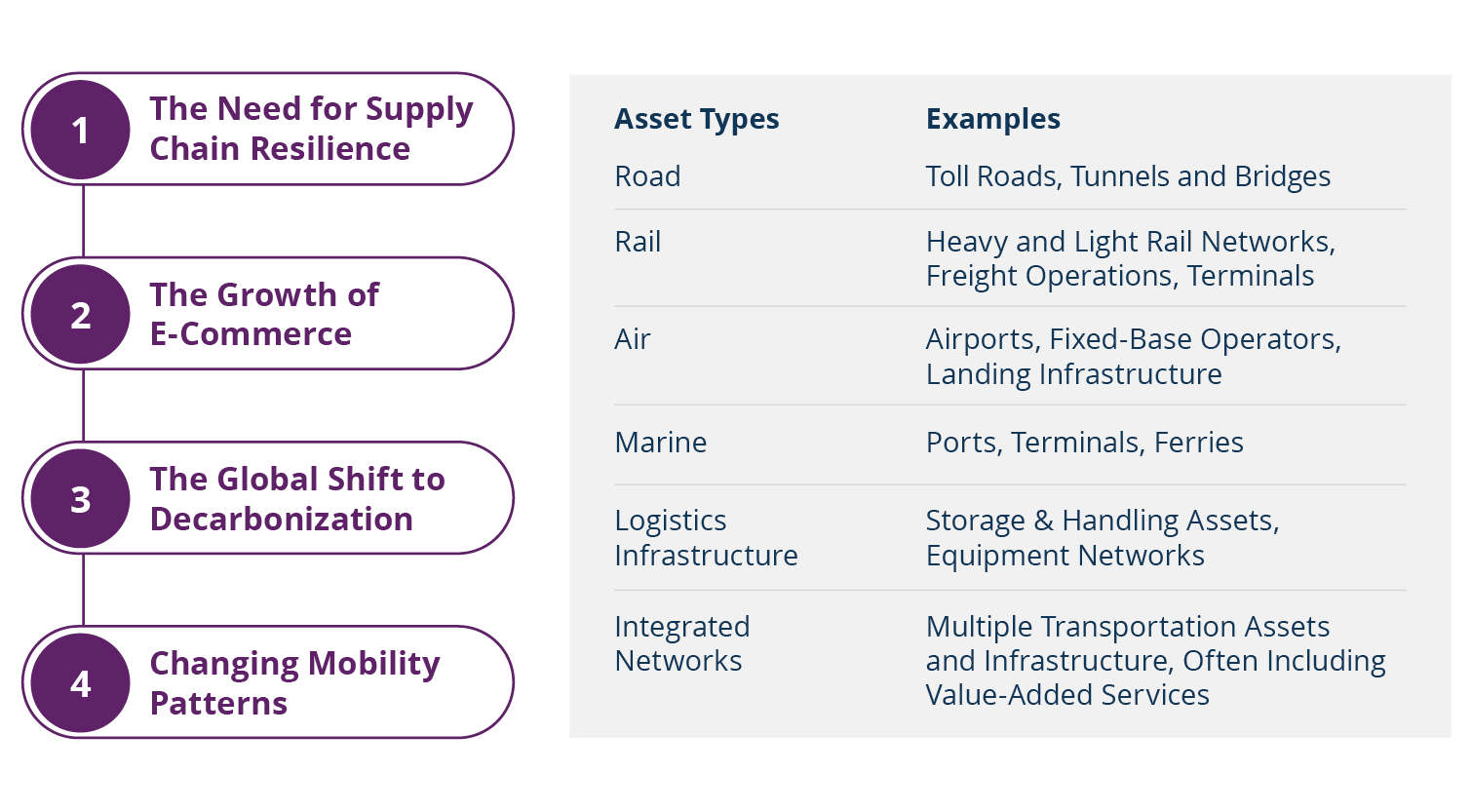

Yet, supply chain resilience is just the first big theme to watch in this space (see Figure 1). As e-commerce continues to grow and fundamentally changes the way goods move, transport logistics businesses will need to adapt. These businesses will also need to “green up” their assets and networks to meet emission reduction targets and emerging environmental regulations as global decarbonization initiatives take hold. Finally, changing mobility patterns will require advances in technology to unlock new time-saving and cost-effective options, catering to evolving passenger preferences.

Critical transport assets—road, rail, air, marine, logistics infrastructure and integrated networks—require substantial capital to eliminate inefficiencies, increase network capacity, decarbonize and provide greater reliability.

Investments are necessary to make supply chains more resilient—and to address significant expected changes in e-commerce, decarbonization and mobility. The last few years have also demonstrated the critical role logistics equipment networks play in global supply chains. But from an investor’s standpoint, large capital requirements often create attractive opportunities.

In addition, today’s elevated inflation and tight commodity environment further underscore the critical nature of transport infrastructure to the global economy—and the need for further investment.

Figure 1: Four Themes to Watch in Transport Infrastructure

Key Themes

The Need for Supply Chain Resilience

Over the last several decades, manufacturers embraced “just-in-time” manufacturing, where parts were delivered to factories as they were required, minimizing the need to stockpile them.

This allowed manufacturers to stay nimble and cut costs. But when the Covid-19 pandemic hit, supply chains struggled to keep up with rising demand as factories shut down and global trade was disrupted.

As a result, manufacturers are now shifting to a “just-in-case” inventory model, and tenants of logistics facilities are looking to secure more warehouse space to accommodate this safety stock. Consequently, inbound and outbound transportation networks will need to be rebuilt to provide redundancy, flexibility and security.

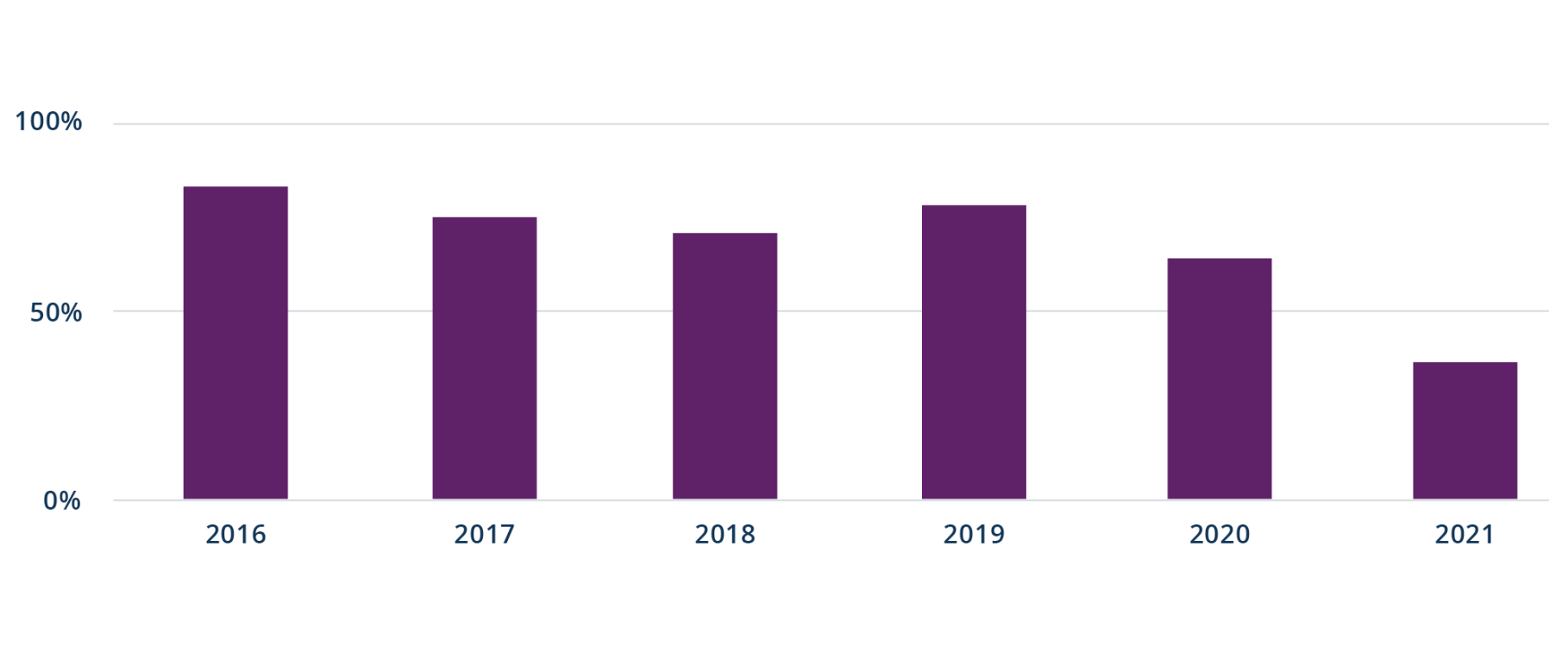

Approximately 90% of world trade moves by sea; yet, because of backups and delays, the movement of freight using existing infrastructure and equipment slowed significantly during the pandemic (see Figures 2 and 3). This meant that high demand for goods met labor disruptions at ports, warehouses and trucking companies—causing reduced asset throughput and turn times, which tightened available capacity and resulted in a backlog.

Figure 2: The Percentage of Shipping Vessels Arriving on Time Has Plunged…

Figure 3: …While Ports Have Remained Congested

Port Congestion Index, % Difference Between Current Level and Five-Year Avg.

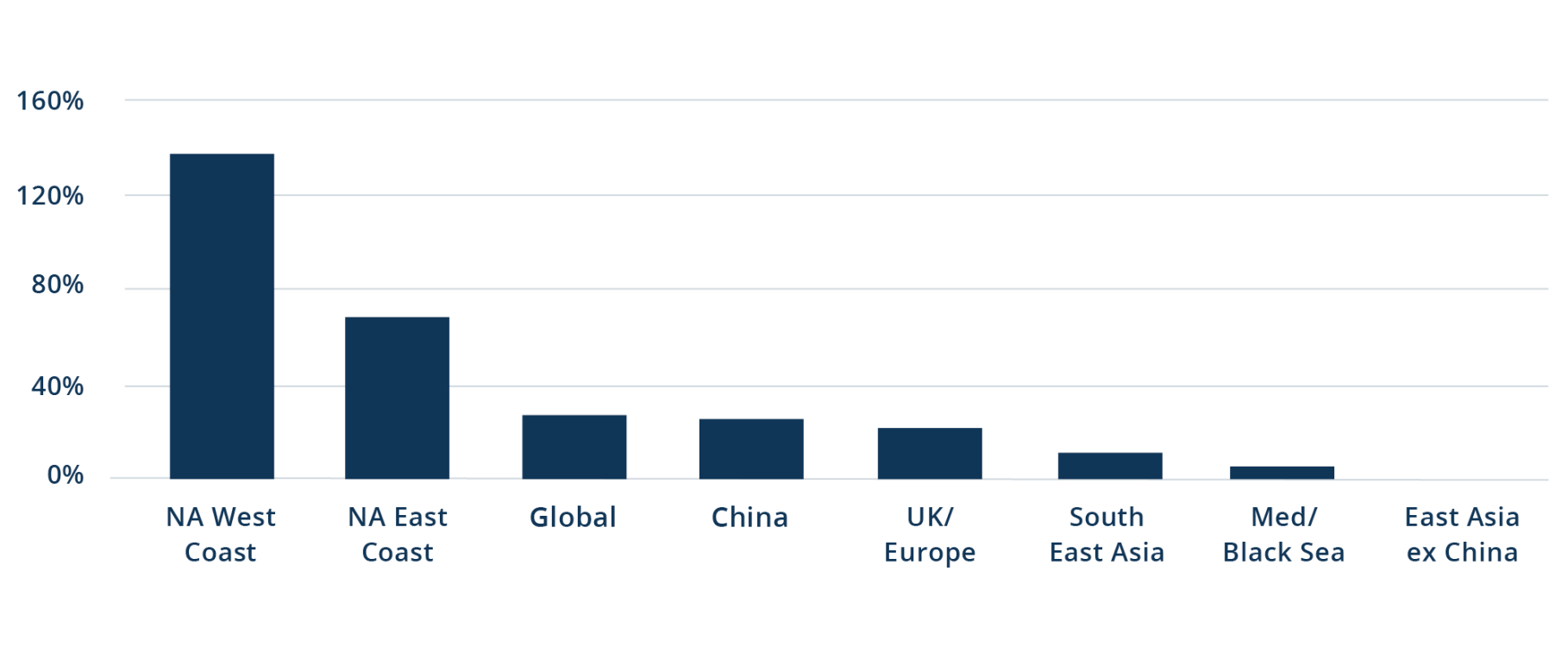

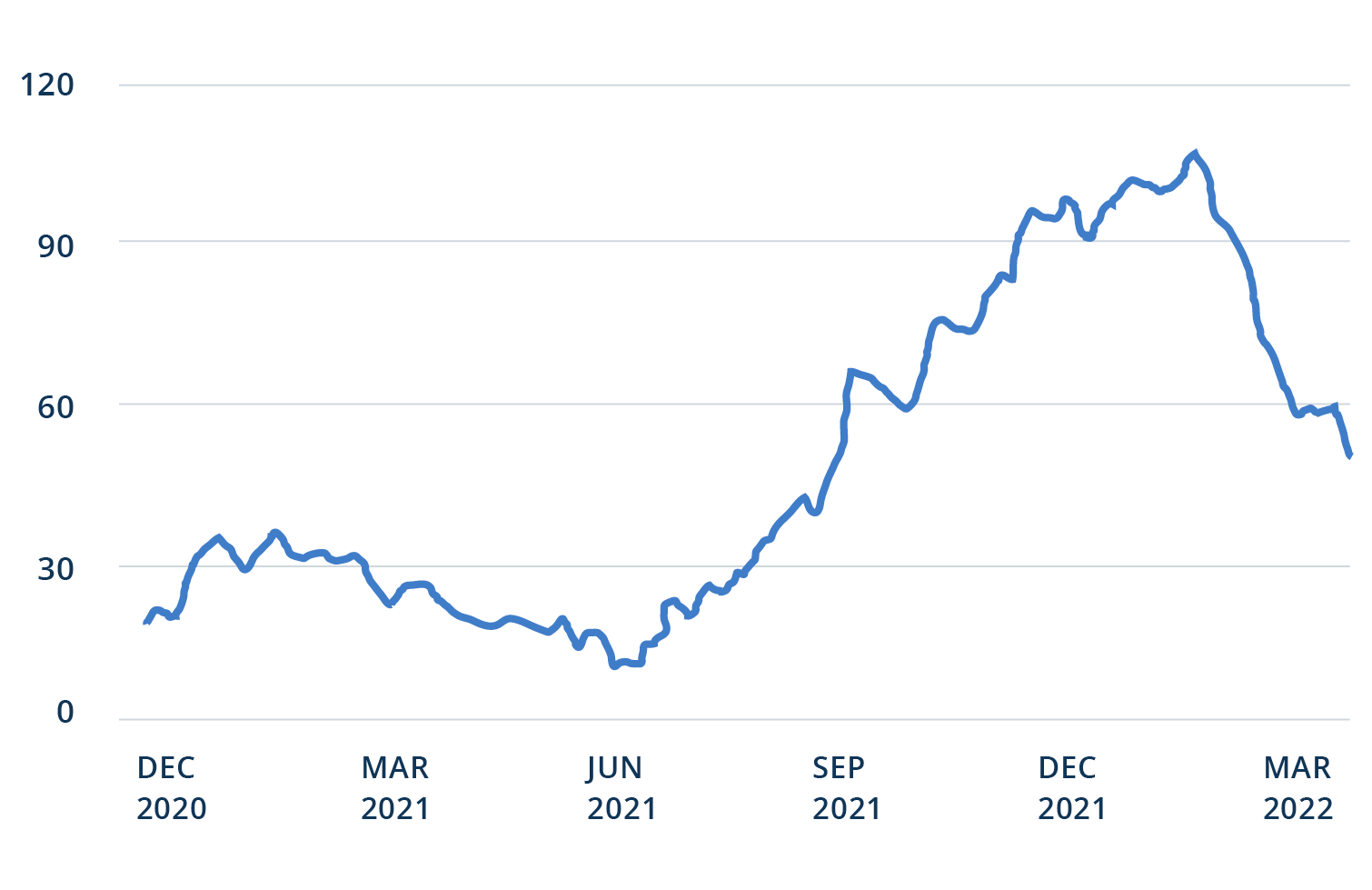

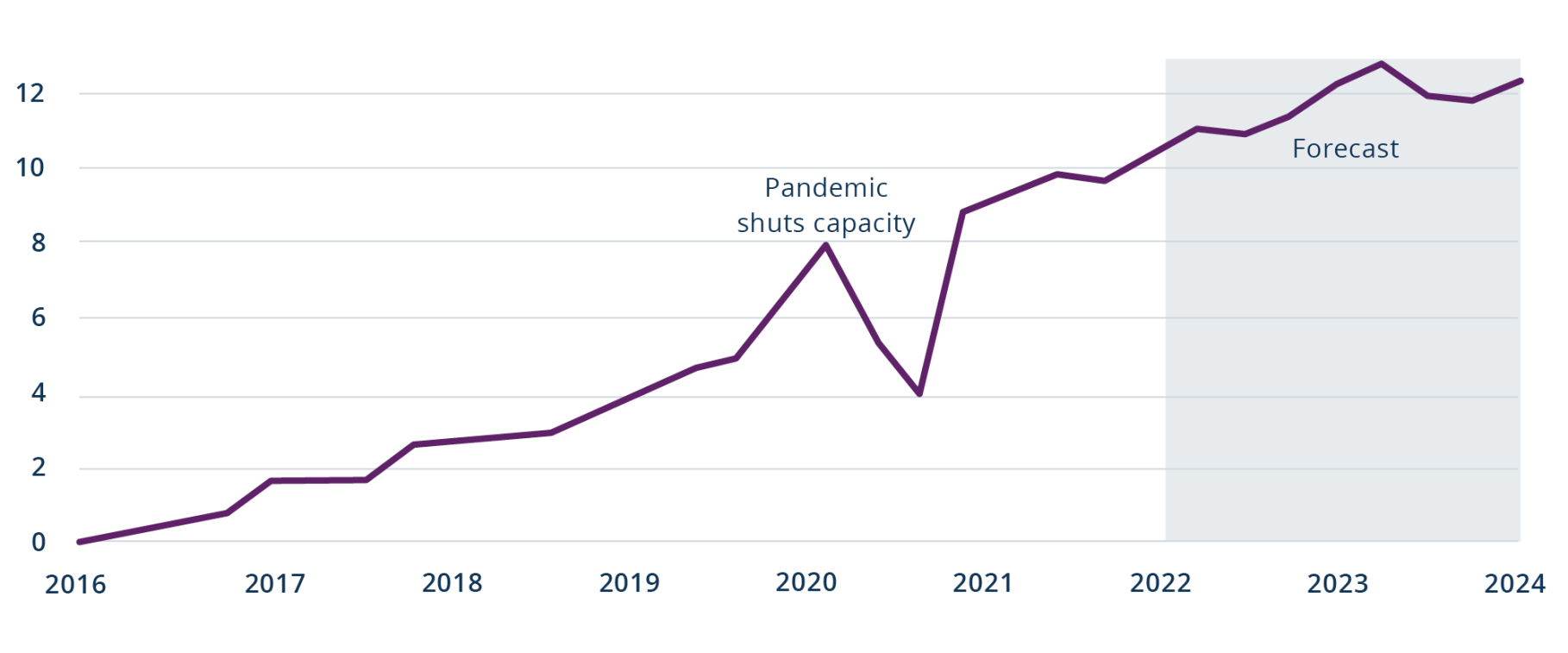

With lower asset utilization, the price of capacity—for shipping, rail, air and trucking—has jumped higher (see Figure 4).

For example, at the U.S. ports of Los Angeles and Long Beach—key U.S. gateways for Asian imports—outdated infrastructure and an inability to operate 24/7 at some terminals have contributed to severe congestion. In fact, the number of vessels lined up outside those terminals has become a barometer of worldwide supply chain disruption. That queue still exists, but the number of vessels waiting today is now more than 50% lower than the January 2022 peak (see Figure 5). Nevertheless, customers have been willing to pay a significant premium for guaranteed capacity—and from a long-term perspective, are looking for ways to control more of their inbound supply chain.

To make ports more resilient in managing such volumes, they will need to modernize and become more efficient through technology and automation. To make these improvements on a global scale, more investment is needed in agile, tech-enabled logistics and supply chain infrastructure. Brookfield’s investments in Patrick Terminals, Australia’s largest container terminal operator, and TraPac, a U.S. west coast container terminals business, provide examples of this approach. The Port of Rotterdam in the Netherlands is another example.

Figure 4: The Price of Capacity Has More Than Tripled in Two Years

Global Freight Rate Index

Figure 5: Congestion Is Easing at the Port of Los Angeles/Long Beach

No. of Anchored/Loitering Ships

The Growth of E-Commerce

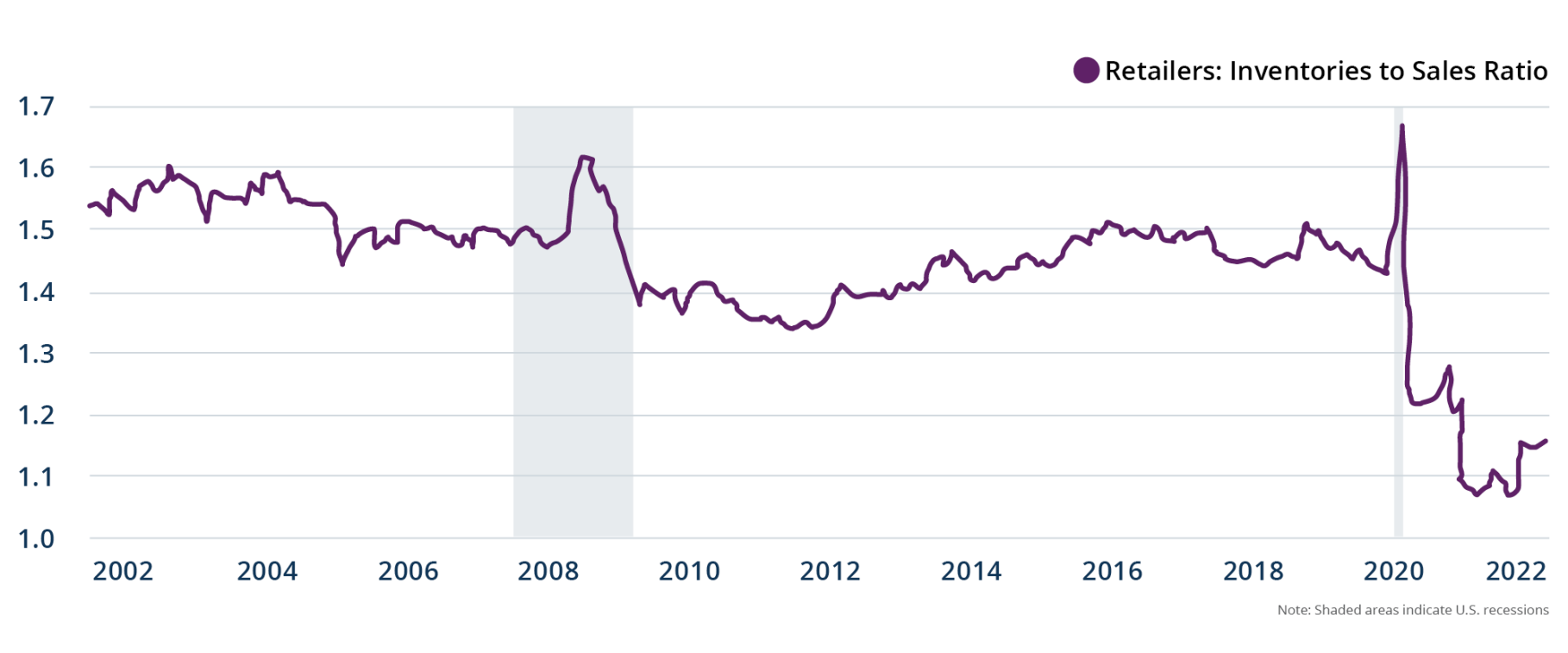

For years, supply chain managers sought to reduce inventories. However, the pandemic accelerated a shift in spending, with consumers spending more on goods—especially online—and less on services.

Consider the ratio of inventories to sales, which indicates the number of months of inventory that are on hand relative to the sales for a month. After averaging 1.47 from 2015 to 2019, this ratio has declined significantly since the start of the pandemic to 1.16 as of March 2022 (see Figure 6).

Online activity puts tremendous pressure on transportation networks. It requires a high degree of supply chain dependability, faster “speed to market” and a shortening of supply chains. A generation of consumers has come to expect that almost anything they order online can be delivered the same day or overnight, underscoring the criticality of last-mile delivery networks.

Meeting those expectations will require reevaluating the importance of inventory buffers and the location of critical assets, considerations that are beyond cost. As a result, companies like Amazon and Walmart are increasingly interested in owning critical infrastructure to help secure their supply chains as they review how goods are moving from Point A to Point B.

As e-commerce penetration levels continue to increase, current inventories need to be boosted significantly, above pre-pandemic levels. And much of the transportation networks, software and systems must be updated and redesigned for this new reality.

Figure 6: More Inventory Is Needed

A generation of consumers has come to expect that almost anything they order online can be delivered the same day or overnight, underscoring the criticality of last-mile delivery networks.

The Global Shift to Decarbonization

The growing urgency around decarbonization has pushed many transport firms to announce—and accelerate—net-zero targets.

For example, Maersk, the world’s second-largest shipping line by container capacity, is bringing forward a target to cut carbon from its operation by a decade—to 2040, instead of 2050, as it responds to growing demand from companies such as Amazon, Ikea and Unilever for an emissions-free supply chain.1 In the coming years, many transport businesses will need to invest substantial capital to transition their assets and business models to meet emissions targets and emerging environmental regulations.

The transport sector accounts for approximately 24% of all CO2 emissions worldwide2 and will need to reduce those emissions by two-thirds to meet a 1.5 degrees Celsius warming scenario by 2050.3

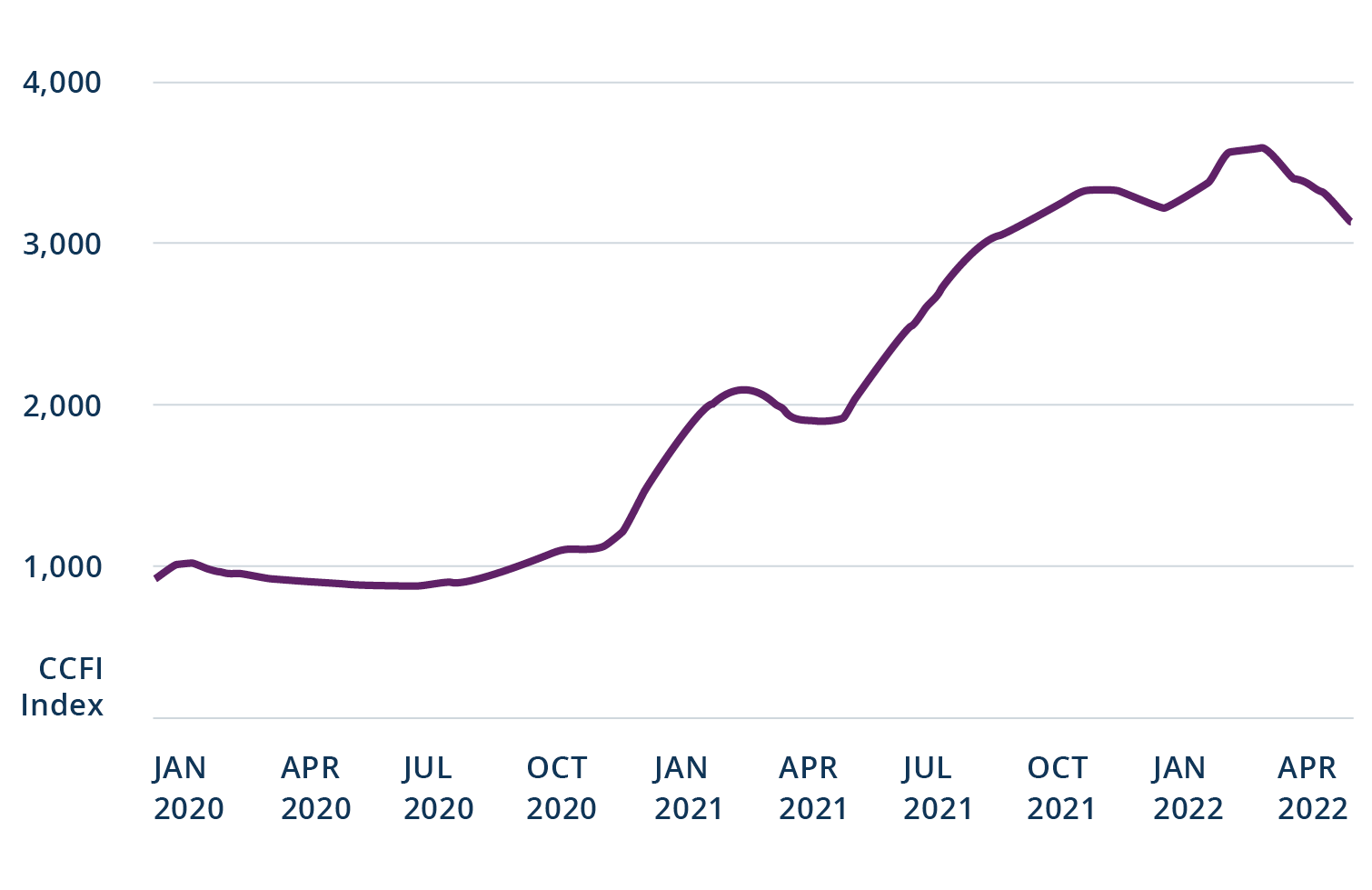

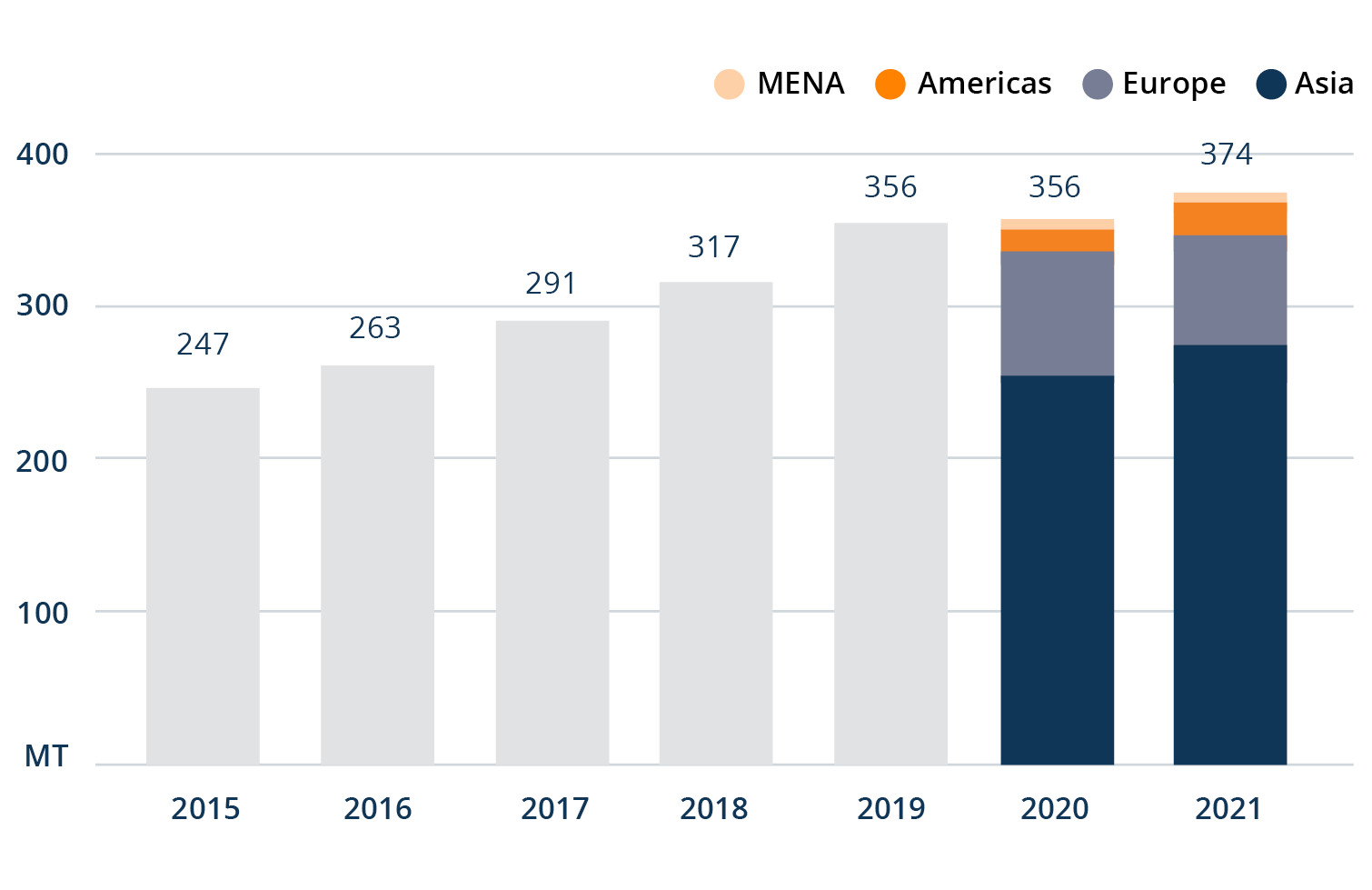

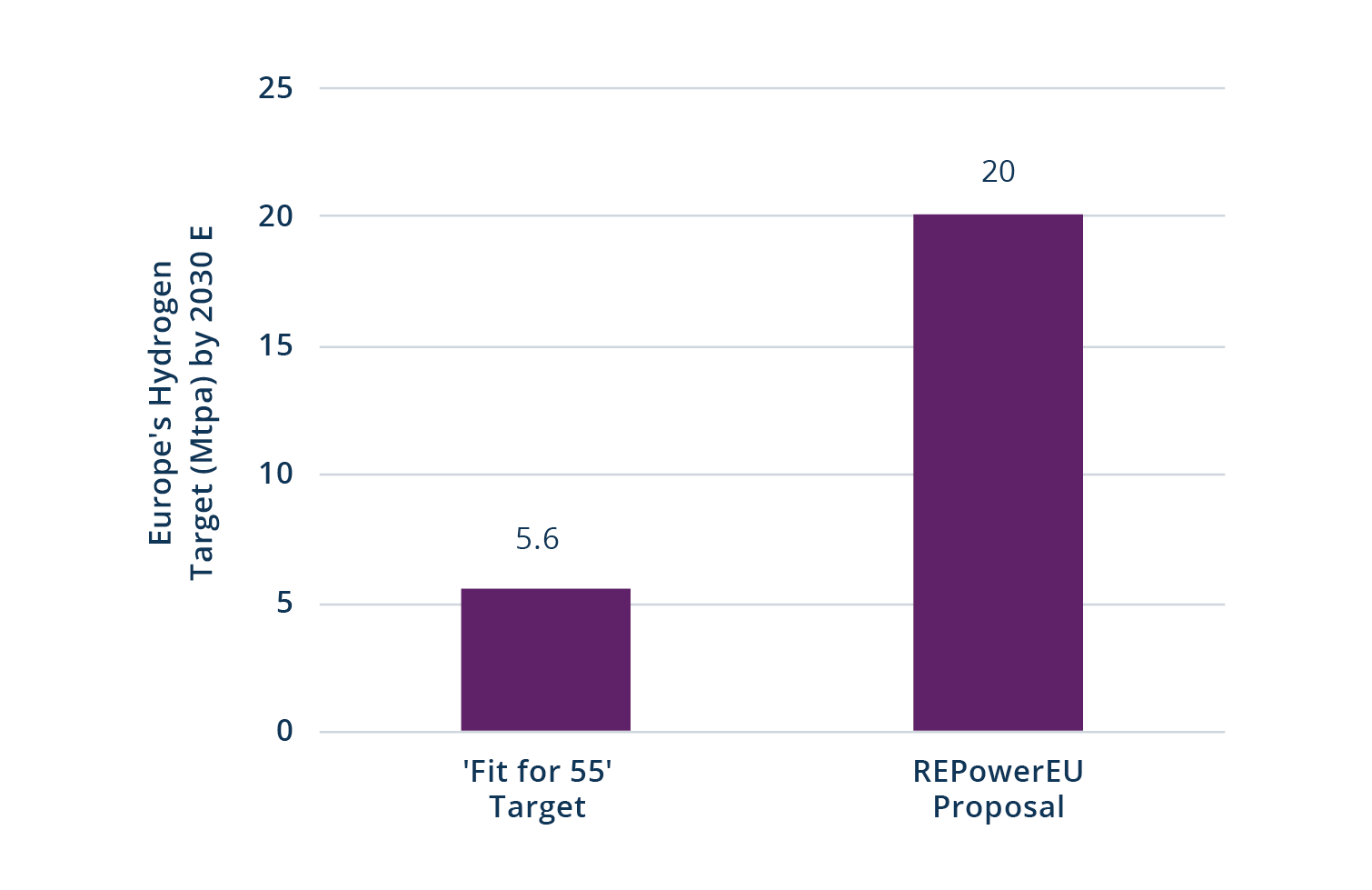

At the same time, as the energy transition accelerates—and as security of energy supply increasingly factors into the conversation—demand is rising for the transportation and storage of lower-carbon-emitting commodities, such as natural gas and hydrogen (see Figures 7 and 8).

Figure 7: Demand Is Trending Up for Liquefied Natural Gas

Figure 8: Europe’s 4x Upgrade to Green Hydrogen Production by 2030

“Desperate to wean itself from Russian oil and gas,” the Financial Times remarked on April 13, “and wilting under soaring energy prices, Europe has rediscovered its thirst for American LNG” (see Figure 9).4

Emissions reduction targets can be achieved through a combination of electrification, advanced fuels and improved materials. For example, a container terminal at a port will need to replace diesel-fired equipment with zero-emissions cargo handling equipment. Furthermore, transport equipment (e.g., ships, trains and planes) will also need to move away from diesel. Energy sources such as hydrogen biofuels will be a critical alternative option for heavy modes of transport, whereas electrification may serve as the more economic and environmental solution for lighter transport vehicles.5 Biofuels are also likely to play a role in the beginning phases of the energy transition.

Positioning these assets for the modern energy economy represents a significant opportunity. In working to “green up” their logistics networks, companies will seek providers of energy-efficient forms of transportation infrastructure with capital and operating expertise.

Figure 9: U.S. Liquefied Natural Gas Exports Are Forecast to Continue Rising

Cubic Feet Per Day (Bil.)

Changing Mobility Patterns

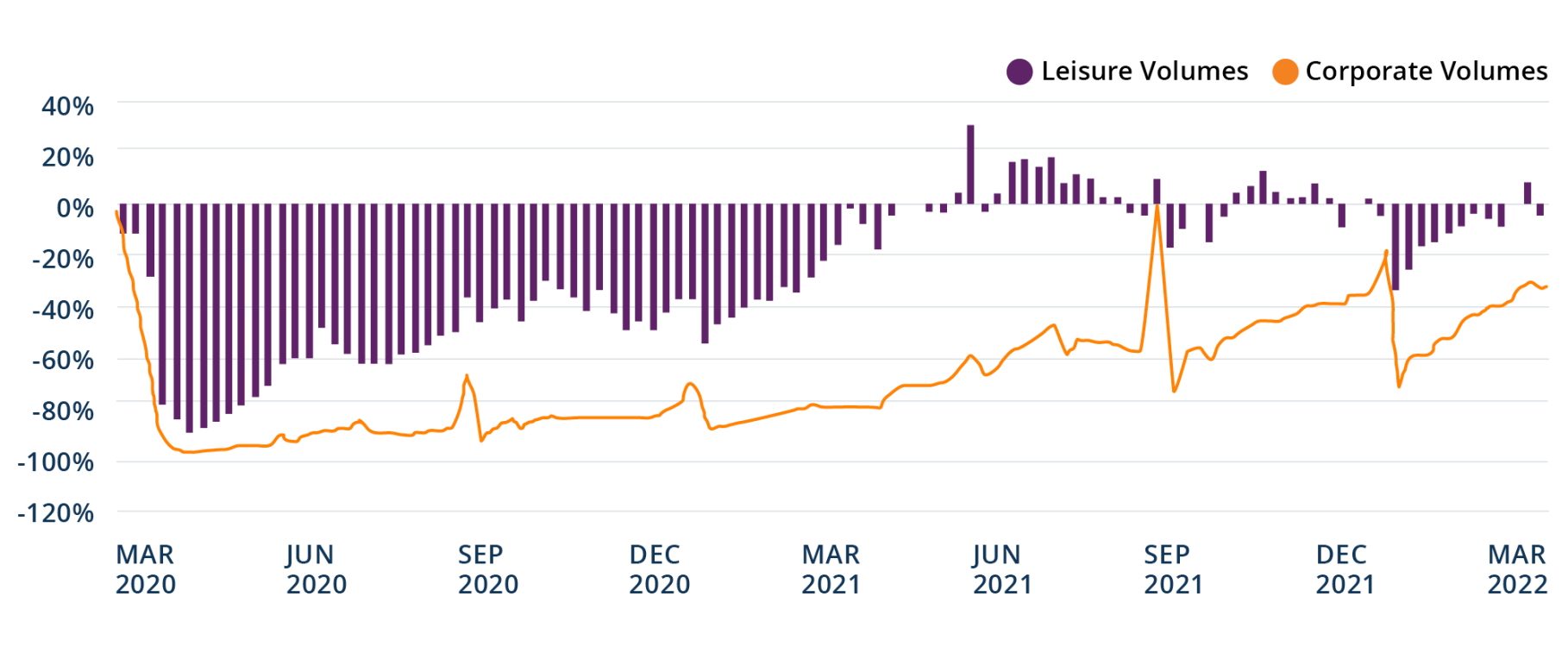

The pandemic shifted mobility patterns, with more time being spent at or near the home—and far less time in the air (see Figure 10).

Even in a post-pandemic future, where and how people travel are likely to evolve, especially with advances in technology. One past example of this is how Uber and Lyft disrupted the taxi industry by leveraging technology to allow users to order cars on their phones, undercutting on price and offering more seamless methods of payment.

Today, technology and digital services are becoming even more important across transportation networks, and recent deal flow in this space illustrates this. For example, in January 2022, Italian toll road group Atlantia acquired Yunex Traffic, a unit of Siemens, for €950 million.6 Yunex provides “intelligent” traffic solutions—such as tunnel automation, smart tolling and adaptive traffic systems for simulation and prediction—in over 600 cities. The transaction demonstrates how current and expected changes in the mobility sector will make it necessary to create new infrastructure and services to manage traffic and control emissions within and outside urban centers.

Advances in technology, and the electrification of aircraft, might also make urban air mobility investable in the years to come—especially if it’s quiet, cheap and safe. The development of electric vertical take-off and landing aircraft could ease urban congestion—especially in growing cities that might be limited by public sector infrastructure.7 Big issues must be addressed before we reach that point, such as public acceptance, as well as certification by aviation regulators. If the urban air mobility industry does take off, the buildout of landing infrastructure—perhaps on the top of multistory parking garages or office buildings—will be required.

Figure 10: U.S. Corporate Air Travel Remains ~33% Below 2019 Levels

Ticket Volume Growth

Conclusion

The past few years have highlighted the importance and critical nature of transport infrastructure. To bolster current networks, additional capacity and substantial investment will be required, driven by the key trends influencing the sector—including supply-chain challenges, the continued growth of e-commerce, the shift to decarbonization and increasing mobility. Because many governments now have heavily indebted balance sheets, the private market is poised to play a prominent role in providing much-needed capital.

Critical and stable infrastructure assets may benefit from many of the macroeconomic trends that are prevalent in today’s markets, including higher volumes, rising inflation, strong commodity prices and reduced capacity due to supply chain bottlenecks.

Essential and large-scale transport infrastructure businesses have other advantages. They generally have a preferred and captive geographic location or corridor, high initial fixed-cost investment and low non-variable operating costs. These attributes can result in high margins and significant barriers to entry. For example, mature toll road assets, according to a December 2021 report from BofA Global Research, typically report EBITDA margins in the range of 60–75%, with some assets exceeding 80%.8

And despite the congestion, the Port of Los Angeles last year broke its 2018 record for annual containerized imports by 13%.9 Container terminal business can still benefit when there are delays—for example, by collecting additional demurrage revenues. Finally, when the demand for logistics infrastructure is high, scaled businesses can realize higher tariffs as customers compete for limited capacity.

As with any investment, there is always risk to consider. For example, transport infrastructure is often GDP-sensitive, with revenues driven by economic growth. However, the essential nature of the assets, strong pricing power and a positive long-term demand outlook tend to mitigate this risk.

Looking ahead, we expect transport infrastructure companies to increasingly seek partners who can provide capital, along with operational expertise, and have seen the durability of these assets first-hand through different economic cycles and periods of disruption. These are the tools they will need to build stronger, resilient assets and larger, more efficient networks.

Endnotes:

1. Maersk, “A.P. Moller - Maersk accelerates Net Zero emission targets to 2040 and sets milestone 2030 targets,” 12 January 2022.

2. International Energy Agency (IEA), “CO2 emissions by sector, World 1990-2019.”

3. International Transport Forum, “ITF Transport Outlook 2021.”

4. Financial Times, “Biden and Ukraine: from climate champion to oil price panic,” 13 April 2022.

5. Shell, Deloitte, “Decarbonizing road freight: Getting into gear” 2021.

6. Atlantia, “Atlantia agrees acquisition of Yunex Traffic from Siemens,” 17 January 2022.

7. Financial Times, “Air taxis: flight of fantasy or truly set for lift off?” January 30, 2022.

8. BofA Global Research, “Launching on Infrastructure: Entering a €2tn stimulus ‘Golden Era,’” 10 December 2021.

9. Port of Los Angeles, “Port of Los Angeles Breaks Cargo Record in 2021, Sets Priorities for 2022,” 20 January 2022.

Disclosures

This commentary and the information contained herein are for educational and informational purposes only and do not constitute, and should not be construed as, an offer to sell, or a solicitation of an offer to buy, any securities or related financial instruments. This commentary discusses broad market, industry or sector trends, or other general economic or market conditions. It is not intended to provide an overview of the terms applicable to any products sponsored by Brookfield Asset Management Inc. and its affiliates (together, "Brookfield").

This commentary contains information and views as of the date indicated and such information and views are subject to change without notice. Certain of the information provided herein has been prepared based on Brookfield's internal research and certain information is based on various assumptions made by Brookfield, any of which may prove to be incorrect. Brookfield may have not verified (and disclaims any obligation to verify) the accuracy or completeness of any information included herein including information that has been provided by third parties and you cannot rely on Brookfield as having verified such information. The information provided herein reflects Brookfield's perspectives and beliefs.

Investors should consult with their advisors prior to making an investment in any fund or program, including a Brookfield-sponsored fund or program.

No comments:

Post a Comment